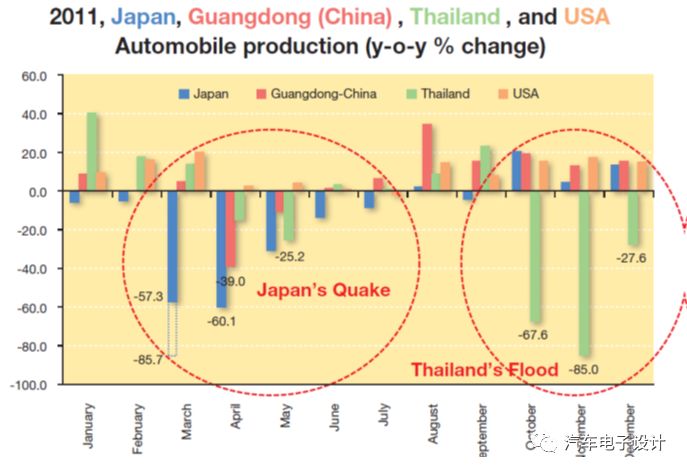

The two-day hot spot is ZTE's business. However, this point definitely shows one thing. It goes down and down. In the process of continuous electronicization of automobiles, whether it is due to similar trade wars or earthquakes or floods, the supply chain The threat is traceable and real. As shown below

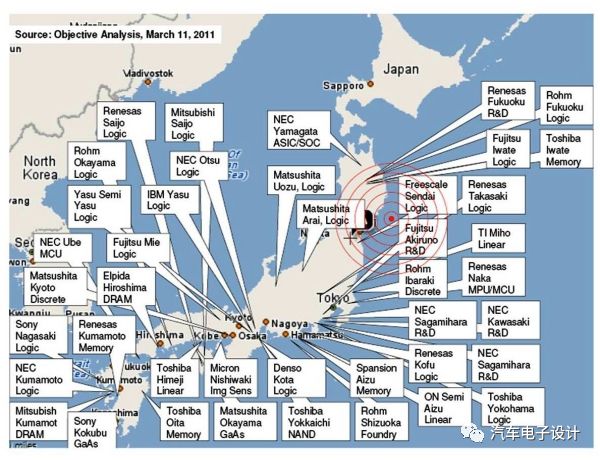

Take the Japan earthquake as an example. At that time, it had a very direct impact on the semiconductor supply in Japan. This directly led to the strict control of Japanese and American car companies on the supply chain.

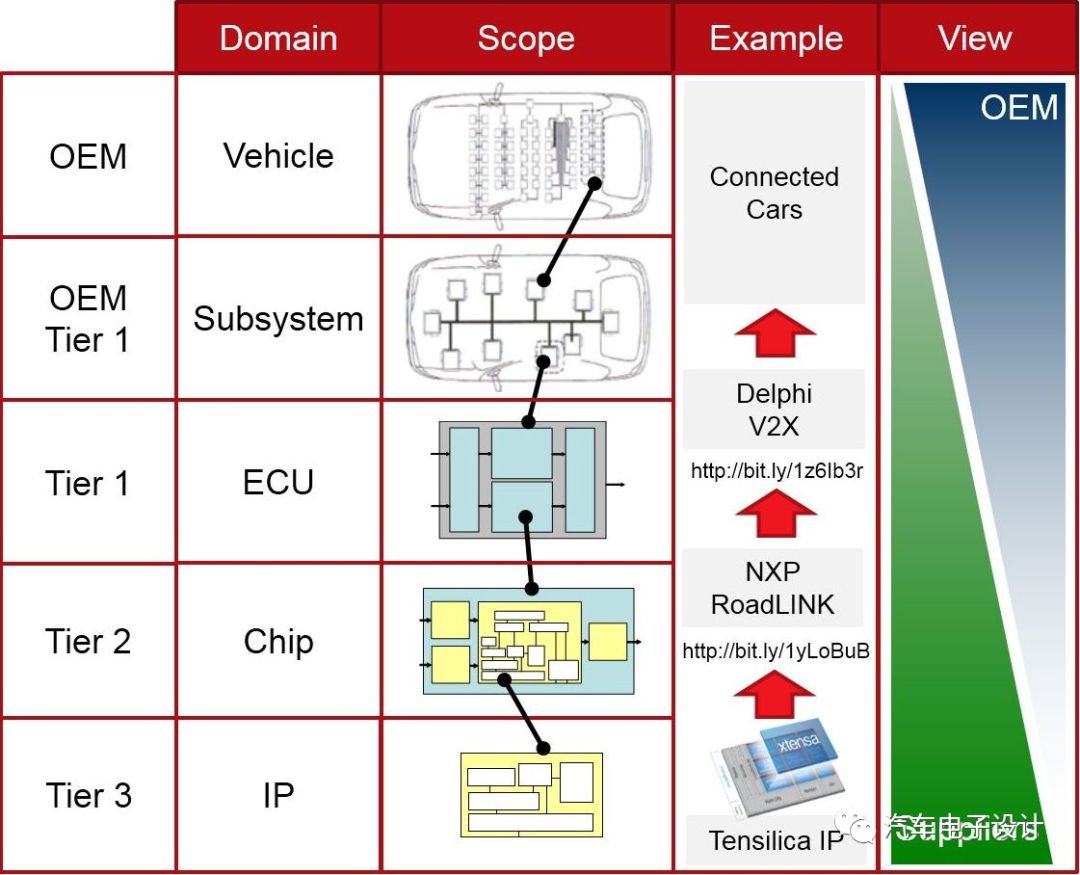

For a car that needs a lot of industrial chain collaboration, it also needs to consider certain game issues in addition to the cost price. As we are sinking, one side needs to review the assembly and subdivide it into the ECU. It may also need to review the supplier strategy of the core device.

In automotive electronics, because different parts do not have the same requirements, they actually go slowly. However, for the product's failure rate, the problems are very important.

In 1998, the automotive market accounted for 7% of the global semiconductor market, until 2015, the market share only slowly increased to 9-10%

Remarks: The oldest American is the first communication company in our communication network. Behind the computer, mobile phone and car electronics, we have to fight it.

Market size 33 billion US dollars

The automotive electronics semiconductor market has been at a stable stage of development for a long time, so there are not many players to come in. There is a problem we can compare with the sales of the entire automotive industry, and sometimes it is somewhat disproportionate.

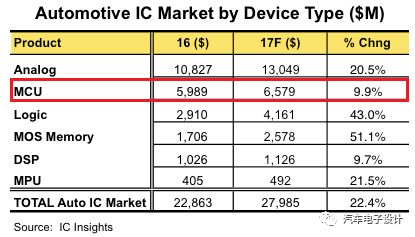

Take MCU as an example

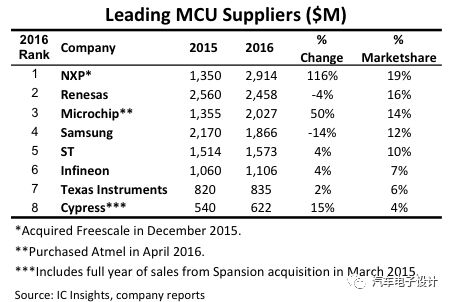

From 2015, several large-scale mergers and acquisitions took place between major MCU vendors in order to compete for market share. According to the statistics of IC Insights, a market research organization, the sales of NXP, Microchip, and Cypress MCU product lines increased significantly year-on-year and the rankings increased accordingly.

MCU vendors that have not made large-scale acquisitions are flat, with only single-digit growth, such as ST and TI, and some have dropped significantly, such as Samsung. The total market share of the 8 MCU vendors reached 88%, and the MCU market will reach its peak in 2020 with sales of US$20.9 billion.

The problem of the MCU is, on the one hand, that the IP core of the MCU is expanded into the MEMS. On the one hand, the MCU expands in various levels of intelligence and becomes more and more widely distributed.

The automotive electronics industry chain has basically decided to focus on the original players. After Qualcomm acquired NXP, Texas, Osmi, and Microchip, this is not good news.

The demand for chips from individual automakers is low. The demand of a single car manufacturer for a single chip manufacturer is much lower than the demand for hundreds of millions of products such as smart phones. There is a demand for customized automotive chips, and semiconductor companies rarely have direct business contact with automakers. Most of them supply components through suppliers.

High requirements for product reliability and longevity: The car's use environment is very harsh, and it usually works in extreme temperatures, high humidity and harsh environments, plus the car's zero-tolerance requirements for safety accidents, and the ability to resist semiconductor products. Reliability and stability requirements are extremely high. The replacement frequency of automotive products is very low, and the service life of the vehicle is close to 20 years, which places high demands on the long-term supply capability of semiconductor companies.

Long product certification cycle and strict standards. The AEC-Q100 standard of the Automotive Electronics Association (AEC) and the ISO-26262 standard of the International Organization for Standardization (ISO) have extremely high requirements for the safety and reliability of automotive electronics. Semiconductor manufacturers obtain relevant certifications before they can enter the automotive industry chain.

Semiconductor companies, parts suppliers, and vehicle manufacturers have formed strong binding supply chain relationships and constitute solid industry barriers for new companies. And the entire semiconductor industry has been buying and buying from 2016 to 2017

Transferred from Non-network "taking stock of eight semiconductor acquisitions in 2017"

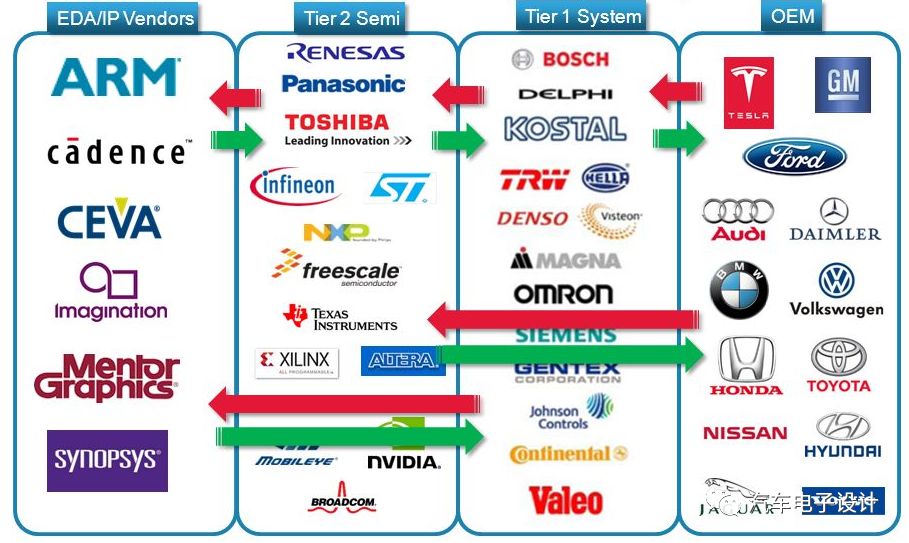

For us at the board level, this matter is really not very good control, this thing is not so simple to invest money to do it, and now many auto companies are deep into the Tier2 Semi even semiconductor tool level

Compared with the above figure, we can look down and the future of automotive electronics is the bloodline of the automobile, from the competition at the mechanical and material level, to the fusion of some chips and IP.

Summary: I didn't understand what we would do in the future, but I have to think of a solution. Everyone said? What can we do?

Cbd Vape Products Oem,D8 Vape Pen Oem,Cbd Disposable Vape Pen Oem,China Cbd Vape Products Oem

Shenzhen MASON VAP Technology Co., Ltd. , https://www.cbdvapefactory.com